Education Savings Accounts represent a significant shift in how families approach learning choices. These state-funded education accounts give you direct control over your child's education funds, with 21 programs now serving families across 18 states.

As you weigh the pros and cons of ESAs, you'll discover they open doors to diverse educational options, from private school tuition and tutoring services to specialized learning programs and online courses.

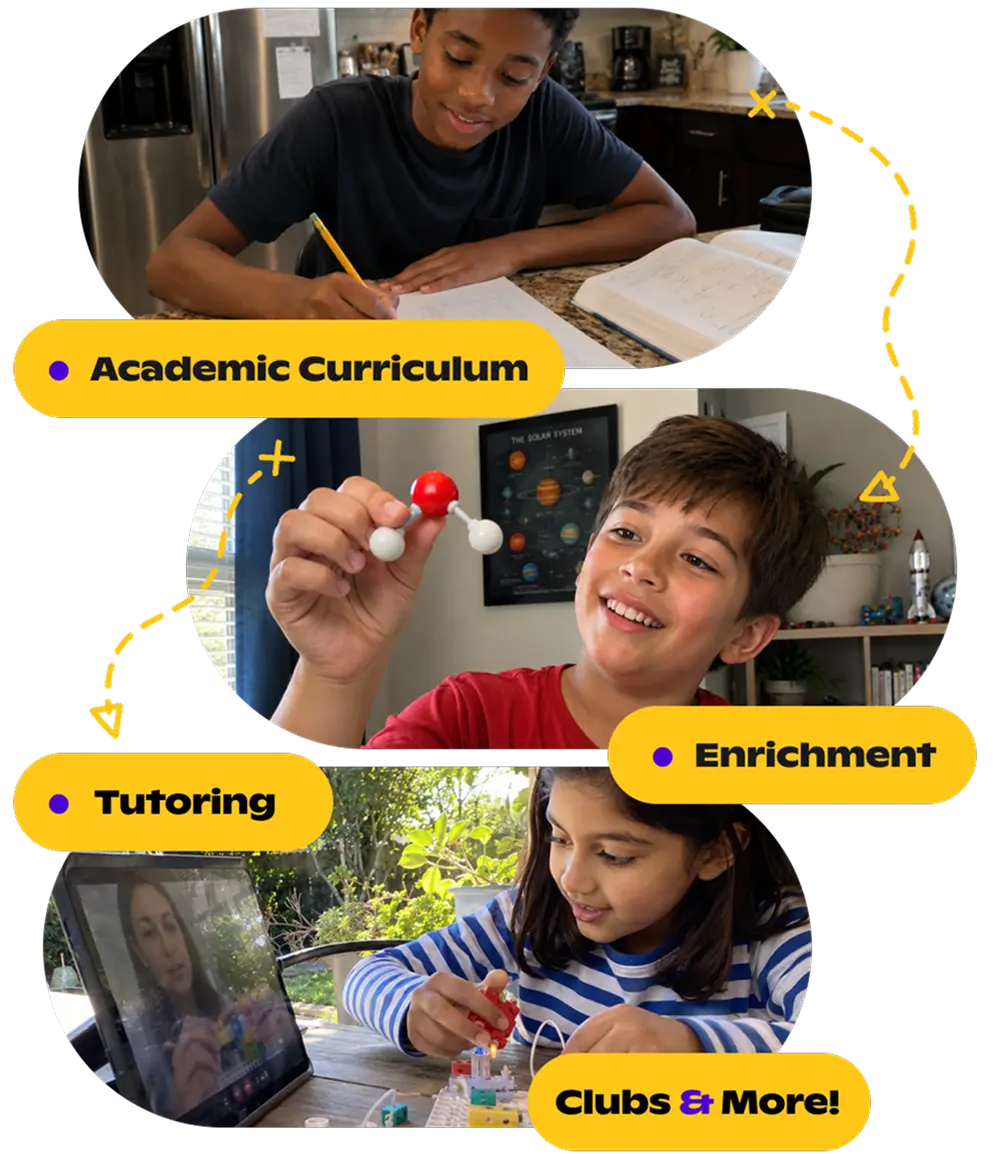

ESAs provide meaningful support for building a personalized education path. Your child can benefit from a mix of learning experiences that match their interests and goals. In select states, this includes using ESA funds for live, interest-led classes on Outschool. With expert-taught options across core subjects, enrichment, and life skills, you can use your ESA funds to boost meaningful, learner-driven progress.

What is an Education Savings Account?

An Education Savings Account (ESA) is part of a growing school choice movement that gives families more control over how, and where, their child learns. The idea is simple: instead of education funding going straight to a public school, the money follows the student.

With an ESA, eligible families receive a portion of their state’s per-pupil funding in a dedicated account, which can be used for approved learning expenses like private school tuition, curriculum, tutoring, or educational tools.

Note: Every ESA program is state-run, with its own name, rules, and eligibility requirements—so what’s covered (and how you apply) can vary widely depending on where you live.

Advantages of Education Savings Accounts

Education Savings Accounts come with several practical benefits that can help families create a more tailored and flexible learning experience for their child. Here are some important ones to know:

- Direct access to public education funds: ESA programs allow eligible families to receive a portion of their state's K–12 education funding to use outside the traditional public school system.

- Flexible use of funds: Families can spend ESA funds on approved educational expenses like curriculum, tutoring, online classes (including Outschool in select states), special education services, and learning tools.

- Personalized learning options: Parents can fully customize their child’s education, supporting unique learning styles, interests, or needs through a mix of resources and approaches.

- Portability and rollover: In some states, unused ESA funds can roll over year to year or follow the student if their educational path changes.

- Targeted support for qualifying families: Most ESA programs give priority or enhanced access to students with disabilities, students from low-income households, or those zoned for underperforming schools.

- No tax liability or repayment required: ESA funds are not considered taxable income, and families are not required to repay the state for approved spending.

Limitations and considerations of ESAs

While ESAs offer powerful benefits, they also come with important rules and limitations. Understanding these upfront can help you make the most of your ESA while staying compliant with your state’s program:

- Typically for non–public school use only: ESA funds are intended for students outside the public school system. If your child re-enrolls in a public school, you’ll typically lose access to the account and remaining funds.

- Funding caps vary by state: Most ESA programs limit the annual amount per student, which can affect how you plan and prioritize educational expenses.

- Eligibility requirements may apply: Access is usually limited to residents of the state offering the program, and some states restrict eligibility based on income level, disability status, or prior public school enrollment.

- Moving states can affect eligibility: ESA programs are state-specific, and benefits don’t transfer across state lines. If you move, you may lose your ESA access entirely unless the new state has a similar program and you are eligible to apply.

- Tutors and providers must be approved: Not all educational vendors or service providers automatically qualify. To use ESA funds, tutors, therapists, and platforms like Outschool must be approved by the program.

Navigating ESA eligibility and application

Each state with an Education Savings Account program sets its own eligibility criteria. These may include factors such as residency, income level, previous public school attendance, or specific educational needs. For example, Arizona offers universal ESA eligibility to all K–12 students residing in the state, regardless of income or prior school enrollment.

Once deemed eligible, families can apply through their state's designated process. Many states use platforms like ClassWallet to manage ESA funds, allowing parents to pay for approved educational expenses directly.

Comparing ESAs with other educational funding options

There are a few different ways you can fund your child's education. Each comes with its own guidelines and uses, so knowing how they compare can help you choose what makes the most sense for your family's needs.

Feature

Education Savings Accounts (ESAs)

529 Plans

School Vouchers

Education Tax Credits

What it covers

Tuition, curriculum, tutoring, online classes, special education services, materials, testing, more

College costs; up to $10,000/year for K–12 tuition (in some states only)

Private school tuition only

Tuition, fees, or other qualified expenses (varies by state)

How it works

State deposits public funds into an account for families to spend on approved expenses

Families save money that grows tax-free for education

State pays tuition directly to private schools

Families pay upfront and claim credits when filing taxes

Flexibility

High, supports a wide range of learning paths and services

Moderate – mostly for tuition, with limited K–12 use

Low – limited to private school tuition

Low – limited control; benefits depend on state programs

K–12 use allowed

Yes – designed specifically for K–12 education

Partially – only private tuition in most cases

Yes – for private K–12 schools only

Sometimes – varies by state

Tax treatment

Funds are not taxable; qualified use is tax-free

Earnings grow tax-free; qualified withdrawals are tax-free

Typically not taxed

Reduces tax liability, not direct funding

Understanding how ESAs, 529 plans, vouchers, and tax credits differ can help you make more informed decisions about how to support your child's education.

Frequently asked questions about ESAs

As you explore ESA options for your family, you might have questions about making the most of these funds. Here are answers to help you confidently move forward with your educational choices.

How do I know if my family qualifies for an ESA?

Your eligibility depends on where you live, as each state designs its own program requirements. Some common qualifying factors include:

- Your child's current school situation

- Family income level

- Special learning needs

- Previous public school enrollment

It's always best to check your state's guidelines to confirm eligibility and the rules that apply to specific ESA programs.

How are ESAs different from other education funding options?

ESAs offer more flexibility than traditional school choice programs. While school vouchers only cover private school tuition, you can use ESA funds for various educational expenses, including online classes, tutoring, curriculum materials, and educational therapy services (depending on the program you qualify for). Plus, unlike 529 plans, ESAs are meant to support K-12 expenses exclusively.

Can I use my ESA funds for Outschool classes?

Outschool currently accepts ESA funds from a select number of states. If you reside in Arizona, Arkansas, Florida, North Carolina, South Carolina, Utah, Texas, New Hampshire, or Indiana, you may be able to use your ESA funds to enroll in Outschool classes.

What if my child's interests or needs change during the year?

That's where ESAs shine! You can adjust your educational spending as your child grows and explores new interests. In some states, unused funds typically roll over to the next school year, giving you flexibility to try new learning experiences.

Leveraging ESAs for educational choices

Education Savings Accounts can open up meaningful possibilities for your child's learning, especially when paired with the right tools and support. With programs available in 18 states and growing, ESAs give you the flexibility to build an education plan that reflects your child's interests, strengths, and needs.

Outschool is here to help you bring that vision to life. In participating states, you can use your ESA funds to access thousands of live, small-group classes taught by passionate educators. Whether your learner is diving into algebra, exploring creative writing, or developing real-world skills, Outschool's flexible, interactive classes make it easier to design a path that's truly personalized.

.svg)

.svg)