Today’s families have more options than ever to guide their learners’ educational path.

Coverdell Education Savings Account (ESA) can be a helpful tool for homeschool families, offering tax-free growth and withdrawals for qualified K–12 expenses. While it covers things like curriculum, books, and some online classes, not all homeschool-related costs may qualify, so it’s a good idea to double-check before using funds.

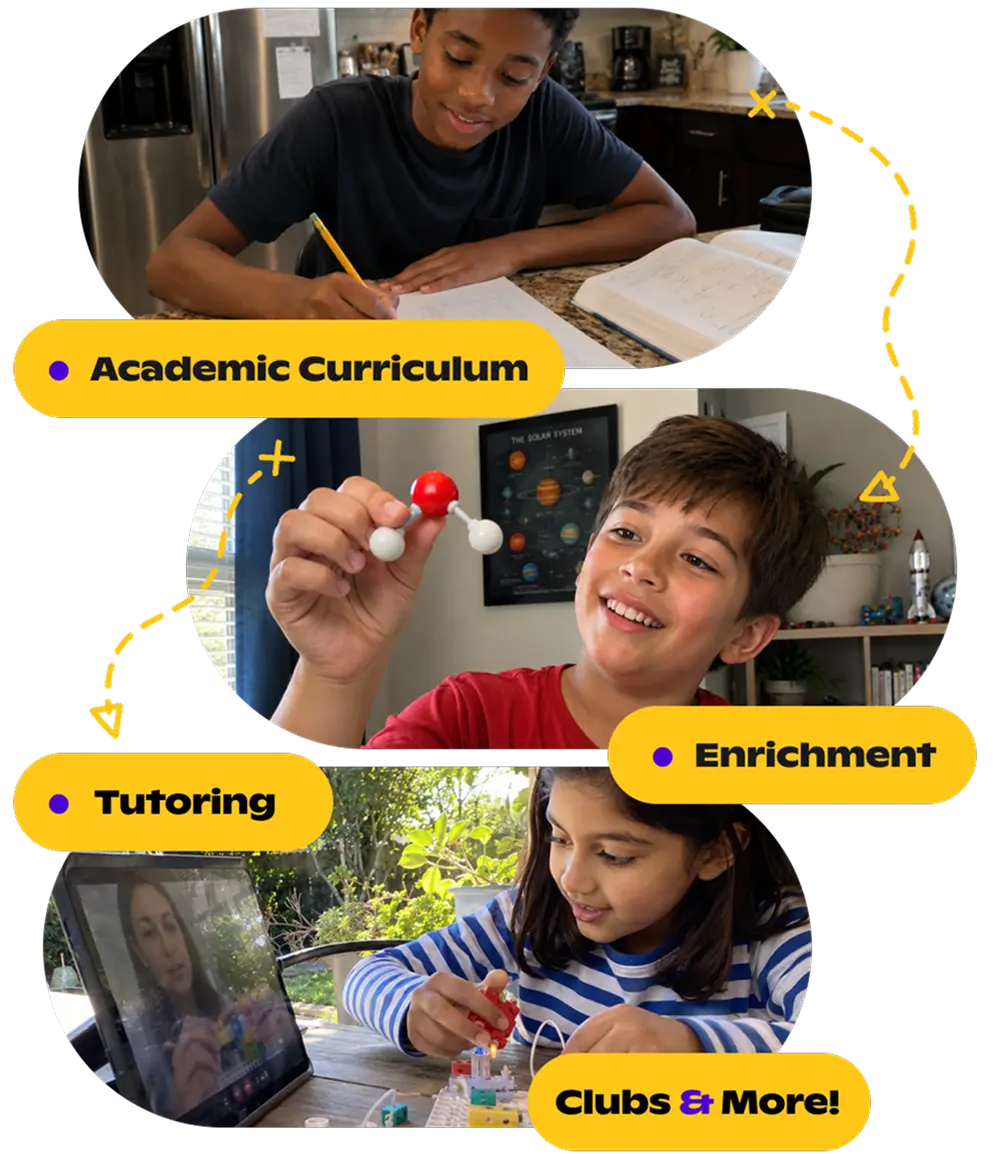

Coverdell ESA withdrawals open the door to many inspiring opportunities when used for qualified education expenses. From academic tutoring to enrichment programs, these tax-free funds can support your child’s growth through platforms like Outschool.

What is a Coverdell ESA?

A Coverdell Education Savings Account (ESA) gives families a tax-advantaged way to invest in their child’s education, from kindergarten through college. Established by the Taxpayer Relief Act of 1997, this account allows contributions to grow tax-free and be withdrawn tax-free, as long as the funds are used for qualified education expenses. These can include various programs, such as those offered by Outschool.

Contribution limits and income eligibility

Each year, families may contribute as much as $2,000 per child to a Coverdell ESA if the contributions are made in cash. You must complete contributions before the beneficiary turns 18, unless they have special needs. Although these contributions aren’t tax-deductible, any earnings grow tax-free within the account.

Eligibility by income:

- Single filers: must earn under $110,000.

- Joint filers: must earn under $220,000.

Contributions begin to phase out at $95,000 for single filers and $190,000 for joint filers.

Families typically withdraw funds during the tax year to cover qualified educational expenses. Many align their withdrawals with school semesters, enrichment programs, or recurring monthly learning schedules.

Qualified vs. non-qualified withdrawals

Not every expense counts when using your Coverdell ESA, but understanding the difference can help you make smart, tax-free decisions. Here's how to know what's allowed (and what isn't).

What learning expenses qualify for tax-free withdrawals?

Qualified withdrawals include:

- K–12 or college tuition

- Academic tutoring

- Required learning materials and technology for educational purposes

- Internet access used for educational purposes

- Room and board (for college with at least half-time enrollment)

What expenses don't qualify?

Expenses like the following are typically not covered:

- Transportation

- Extracurriculars unrelated to academics

- Sports or hobby gear (unless required for class)

- General electronics (not solely for education)

Tax implications of Coverdell ESA withdrawals

When used for qualified education expenses, withdrawals from a Coverdell ESA, including earnings, are entirely tax-free. However, if you use the funds for non-qualified expenses, the earnings portion of the withdrawal becomes taxable, and you may also face a 10% penalty.

Each year, your Coverdell ESA provider will send you Form 1099-Q, which reports the amount of withdrawals. It’s important to keep this form and match it with your receipts and records of education expenses.

Can I use other tax benefits along with a Coverdell ESA?

Yes, but not for the same expense. For example, you could use your Coverdell ESA to pay for tutoring or school supplies, and still claim the American Opportunity Credit for college tuition, so long as you don't apply both benefits to the exact cost.

Careful tracking ensures you don’t double-claim and helps you maximize every available education benefit.

Penalties for improper use

You may face tax consequences if you withdraw Coverdell ESA funds for something that doesn't qualify, like entertainment or non-educational electronics. Specifically, the earnings portion of the withdrawal will be subject to federal income tax and an additional 10% penalty.

However, you won’t owe the 10% penalty if your child:

- Receives a scholarship that reduces the need for ESA funds

- Becomes permanently disabled

- Attends a U.S. military academy

- Passes away

Even when the IRS waives the 10% penalty, you may still need to pay income tax on the earnings portion of a non-qualified withdrawal.

The rules around ESA withdrawals and taxes can be complex. To avoid mistakes and protect your tax benefits, it’s a good idea to consult a tax professional or financial advisor, especially if you're using multiple education savings tools or your situation changes.

$20 off your first class WITH promo code: blog

Build the Education your Kid Deserves

Discover thousands of live classes taught by expert teachers, across academics and enrichment.

Browse classesHow to withdraw funds from a Coverdell ESA

Withdrawing from a Coverdell ESA isn't complicated, but each provider has its own process. Here's what to expect and how to stay organized:

- Contact your Coverdell ESA provider. Contact the financial institution that holds your Coverdell ESA to begin the withdrawal process. Unlike 529 plans, which often have more streamlined online systems, Coverdell ESA withdrawal procedures vary significantly between providers. Some may offer digital portals, like those at Fidelity or Schwab, while others may still rely on paper forms or in-person verification. Always check your provider's current requirements; some may also request proof of identity or documentation verifying the expense.

- Choose who receives the funds. Coverdell ESA distributions can be made payable to you (the account holder), the beneficiary, or directly to an educational institution or qualified provider, depending on how you plan to use the funds.

- Gather supporting documents. Keep receipts, invoices, or enrollment confirmations to show that you used the funds for qualified educational expenses. These records are essential for your tax filing.

- Track and match your expenses. For each withdrawal, ensure a matching qualified expense within the same tax year. This helps maintain the tax-free status of your distribution and avoids unnecessary penalties.

Common mistakes to avoid

Even the most well-intentioned families can face pitfalls when managing a Coverdell ESA. Here are some common missteps to watch for and how to stay on track:

- Overlooking documentation requirements: Always save receipts and enrollment confirmations to show that you used withdrawals for qualified educational expenses

- Spending on non-qualified expenses: Costs like transportation, sports gear (unless required for a class), and general electronics may not be eligible and could trigger taxes and penalties.

- Double-claiming education benefits: Avoid using the same expense to claim Coverdell ESA withdrawals and other tax credits like the American Opportunity Credit.

- Missing the age 30 deadline: Funds must be used or rolled over by the beneficiary's 30th birthday, unless they have special needs. Planning helps you avoid surprise tax consequences.

- Exceeding contribution limits: Contributions over $2,000 per beneficiary per year are not allowed and could result in excise taxes unless corrected promptly.

Special rules for age limits and rollovers

Coverdell ESA funds need to be used or transferred to another eligible family member before the beneficiary reaches age 30, unless the beneficiary has special needs. If funds remain past that age without a rollover, any earnings may be taxed as income and face a 10% penalty.

To protect your ESA's tax advantages, follow these rollover rules:

- Roll over to another eligible family member under 30. Eligible family members include siblings, cousins, nieces, and nephews. This allows the funds to stay within the family and continue supporting a child's education.

- Complete the rollover within 60 days. The IRS requires you to complete the transfer within 60 days of the distribution date. Missing this window could trigger taxes and penalties.

- Limit rollovers to once every 12 months per beneficiary. If you roll over more than once in 12 months for the same beneficiary, the IRS may treat the additional rollovers as non-qualified distributions, potentially resulting in tax and penalties.

- Changing the beneficiary: You can also change the beneficiary to another qualifying family member under age 30 without triggering taxes, as long as the new beneficiary meets the age and relationship requirements.

Frequently asked questions (FAQs)

Families often have specific questions when using ESA funds, especially when choosing between education expenses. Here's a quick guide to help you feel more confident and informed.

What records do I need to prove my Coverdell ESA expenses?

Save receipts, invoices, and enrollment confirmations for each qualified expense. Match every record with the withdrawal made during the same tax year. This is especially important for purchases like laptops or internet service, which the IRS only considers qualified if they primarily support your learner's education.

Can I use Coverdell ESA funds for Outschool classes and tutoring?

Yes! Coverdell ESA funds can be used for qualified educational services, including Outschool's live classes and one-on-one tutoring, as long as the programs support your child's academic growth and learning goals.

Can I use Coverdell ESA funds for private K–12 tuition?

Absolutely. Tuition at public, private, and religious elementary and secondary schools is a qualified expense under Coverdell ESA rules.

What if my learner doesn't go to college?

No problem. You can still use Coverdell ESA funds for K–12 educational experiences. If your child follows a non-traditional path, you can roll the funds over to another eligible family member under 30 or apply them to qualified alternative education programs that match your learner's goals.

Can I use Coverdell ESA funds for a laptop or internet access?

Yes, if those tools are used primarily for your child's education. The IRS requires that technology and equipment expenses be "primarily for the benefit of the beneficiary" to qualify. That means shared family computers or internet used mainly for non-educational purposes might not count. Save receipts and keep documentation that shows how each purchase supports schoolwork or educational programs.

What happens to the Coverdell ESA funds if my child receives a scholarship?

If your child receives a scholarship, you can still use Coverdell ESA funds to pay for qualified education expenses, but you must reduce the amount of qualified expenses by the scholarship amount when calculating tax-free withdrawals.

For example, if your child's total qualified education expenses are $8,000 and they receive a $5,000 scholarship, you can withdraw up to $3,000 from the Coverdell ESA tax-free to cover the remaining costs. Any withdrawals exceeding the adjusted qualified expenses may be subject to taxes and penalties.

Putting your Coverdell ESA to work for your learner

Managing a Coverdell ESA can feel like a big task, but it becomes a powerful way to support your learner's unique educational path with the right approach. With thoughtful planning, you can maximize your savings to fund everything from traditional academics to creative, interest-based experiences.

Every decision you make, whether choosing a class, timing a withdrawal, or organizing your records, helps build a learning experience that's meaningful, flexible, and tailored to your child. And with Outschool, you have a trusted partner ready to support every step.

.svg)

.svg)